When it comes to claiming Universal Credit, the amount of money, savings, and investments I hold can have a direct impact on both my eligibility and the amount I receive.

These financial resources are considered as “capital” and are assessed as part of my claim. Understanding the Universal Credit savings limit is essential if I want to avoid unexpected reductions in my award or, in some cases, disqualification from the benefit entirely.

What Is The Universal Credit Savings Limit?

The Universal Credit savings limit sets out the amount of capital I can hold before my claim is affected.

This includes money, savings, and investments that I own outright or jointly with someone else. The savings limit is a core part of the means-tested nature of Universal Credit.

Capital can include:

- Money in UK and overseas accounts

- Investments such as shares, bonds, and ISAs

- Property I own but do not live in

- Lump sums from inheritance or compensation

The Department for Work and Pensions (DWP) assesses both my personal holdings and any joint holdings with a partner.

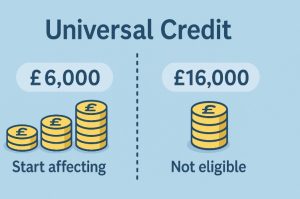

How Much Can You Have In Savings Before Universal Credit Is Affected?

The amount of savings and investments I have plays a direct role in determining how much Universal Credit I receive. Universal Credit uses two main thresholds:

- £6,000 threshold: Any capital below this amount is ignored entirely in the calculation.

- £16,000 limit: If my total capital is at or above this level, I am normally ineligible for Universal Credit altogether.

These thresholds apply to both single claimants and couples. For couples, the DWP will add together my savings and my partner’s savings to get a combined figure, even if one of us is not claiming Universal Credit.

If my savings fall between £6,000 and £16,000, the DWP assumes I am receiving a “tariff income” from those savings. This is not actual interest or investment income but an estimated figure used to reduce my Universal Credit payments.

The formula is:

- For every £250 (or part of £250) over £6,000, £4.35 is deducted from my Universal Credit payment each month.

For example:

- If I have £6,300 in savings, that’s £300 over the threshold. £300 counts as two £250 units (because even partial £250 amounts count as a full unit), which means £8.70 is deducted from my payment.

- If I have £10,000, that’s £4,000 over the threshold, which equals 16 units of £250. My payment would be reduced by £69.60 per month.

- If I have £14,500, that’s £8,500 over the threshold, which equals 34 units of £250. My payment would be reduced by £147.90 per month.

Tariff Income Examples

| Total Savings | Over £6,000 Amount | Units of £250 | Monthly Deduction |

| £6,100 | £100 | 1 | £4.35 |

| £6,500 | £500 | 2 | £8.70 |

| £8,000 | £2,000 | 8 | £34.80 |

| £10,000 | £4,000 | 16 | £69.60 |

| £14,500 | £8,500 | 34 | £147.90 |

| £16,000+ | £10,000+ | N/A | Not eligible |

The DWP looks at savings in a broad sense. It includes:

- Cash in hand

- Money in UK or overseas bank accounts

- Premium Bonds, ISAs, and shares

- Lump sums from inheritance or redundancy

- Property I own but do not live in

This means even if I keep my savings in multiple accounts or investments, they are added together for the purpose of the calculation.

It’s also worth noting that some payments are ignored for a set period before being counted. For example, funds from selling my main home are not counted for six months if I plan to buy another property to live in.

What Happens If Your Savings Exceed £16,000?

Exceeding £16,000 in savings or investments usually means I cannot claim Universal Credit at all. This rule applies whether I am claiming alone or as part of a couple, as combined capital is considered.

There are a few exceptions, such as:

- Moving from tax credits under managed migration with transitional protection

- Some temporary disregards for specific payments

How Does Universal Credit Treat Different Types Of Capital?

When assessing my Universal Credit entitlement, the Department for Work and Pensions (DWP) looks at the total value of my capital. This includes money, savings, investments, and certain types of property.

It applies whether the capital is in my name alone or jointly with another person, and it covers assets both in the UK and abroad.

The rules are detailed because not all forms of capital are treated the same way. Some are counted fully, others are partially disregarded, and some are ignored altogether.

Bank Accounts And Cash

The DWP counts all money I hold in:

- Current accounts (including digital-only accounts like Monzo or Starling)

- Savings accounts with banks, building societies, or credit unions

- Cash I keep at home or elsewhere

Even my main current account, which I use for day-to-day expenses, is included. The only time a bank balance might be excluded is if it contains a temporary disregard payment, such as compensation covered by an exemption.

Savings And Investments

The following types of savings and investments are included in the capital assessment:

- Individual Savings Accounts (ISAs), including cash ISAs, stocks and shares ISAs, Innovative Finance ISAs, Help to Buy ISAs, and Lifetime ISAs

- Premium Bonds

- Stocks, shares, and bonds

- Dividends from investments, if not taken as regular income

- National Savings & Investments (NS&I) accounts

The value is based on the market price at the time of the assessment, minus any transaction costs or debts directly secured against the investment.

Property Other Than My Main Home

If I own property that I do not live in, its value is usually counted as capital. This includes:

- Holiday homes

- Buy-to-let properties

- Land and plots of land

- Caravans and mobile homes

- Property where my name is on the mortgage but I do not live there

Some exceptions apply. For example, if the property is the main home of a close relative who is retired or has a severe health condition, it may be disregarded.

Lump-Sum Payments

Certain lump sums are treated as capital as soon as I receive them, unless they fall under an exemption. Examples include:

- Inheritance

- Redundancy pay

- Pension lump sums

- Divorce settlements

- Large insurance payouts

These must be declared to the DWP straight away. If I spend them on reasonable expenses before the next assessment period, they may not affect my capital total as much.

Business Assets

If I own a business, capital tied up in active business accounts or property used for the business is usually ignored. However, if the business has closed for more than six months, those assets may then count towards my total savings for Universal Credit.

Assets Not Counted As Capital

Some items are excluded from the capital calculation altogether. These include:

- Personal possessions such as clothes, jewellery, furniture, and cars

- Life insurance policies that have not paid out

- Funeral plan contracts

- Savings belonging to children in their own name, such as Junior ISAs or Child Trust Funds

How Are Savings Assessed For Universal Credit?

Savings are valued at their current market value, minus any debts directly secured against them. The assessment includes both UK and overseas assets.

DWP treats unspent income from a previous period as capital in the following period. For example:

- If I earn £1,800 and spend £1,200 before the end of the next assessment period, the remaining £600 is counted as capital.

Savings Assessment Steps

| Step | Action Taken |

| 1 | Add up all money, savings, and investments held in my name or jointly |

| 2 | Include overseas accounts, property, and other assets |

| 3 | Deduct any secured debts from the value of those assets |

| 4 | Apply tariff income rules between £6,000 and £16,000 |

| 5 | If capital is £16,000 or more, check for exemptions or stop the claim |

Do Joint Savings Count For Universal Credit?

If I live with a partner, our savings and investments are added together for the purposes of the Universal Credit assessment. This is the case even if my partner is not personally eligible for Universal Credit.

For example, if I have £4,000 and my partner has £3,000, the DWP treats us as having £7,000 combined savings, meaning the tariff income calculation applies.

How Should You Report Your Savings To Universal Credit?

When I first apply for Universal Credit, I must declare all my capital in the application form. If a type of saving is not listed, I can use the “other savings and investments” section.

I also have a responsibility to report changes as soon as they happen. This includes:

- Receiving inheritance or redundancy pay

- Selling a property

- Large investment gains or losses

If I fail to report these changes promptly, I could be overpaid and later required to repay the amount, potentially with penalties.

Can You Legally Reduce Your Savings To Claim Universal Credit?

I am allowed to spend my savings, but I cannot deliberately reduce them to qualify for Universal Credit in a way that DWP would consider “deprivation of capital.”

Permitted uses of savings include:

- Paying off debts

- Buying goods and services reasonably required for my circumstances

Unacceptable uses include giving money to someone else or making extravagant, unnecessary purchases just to bring my savings below the limit.

What If Your Savings Change While Claiming Universal Credit?

My Universal Credit entitlement is not fixed for the entire time I’m claiming. The DWP reassesses my circumstances each month, which means any change in my savings or investments can directly impact my payments. This is true whether my savings increase or decrease.

When Savings Increase?

If my savings go above £6,000 during a claim, the DWP will apply the tariff income calculation starting from the next assessment period. The higher my savings between £6,000 and £16,000, the larger the monthly deduction.

If my savings reach £16,000 or more, my Universal Credit claim will usually stop altogether from the assessment period in which the increase occurs.

Example:

- My savings were £5,800 in March. In April, I receive an inheritance of £2,500, taking my total to £8,300.

- From May (the next assessment period), the DWP will count £2,300 above the £6,000 threshold. This is 10 units of £250, so my monthly payment will be reduced by £43.50.

It doesn’t matter whether the increase comes from interest, a lump sum, selling property, or other investments all are treated as capital.

When Savings Decrease?

If my savings fall below a threshold, my payment may increase again. For example, if I have £10,000 and spend £5,000 on essential home repairs, leaving £5,000, I will move back below the £6,000 limit and will no longer have a deduction for tariff income.

However, I must be careful. The DWP will look at whether I have deliberately reduced my savings to increase my Universal Credit (this is known as deprivation of capital). Spending must be reasonable and justifiable in my circumstances, such as:

- Paying off debt

- Replacing essential household goods

- Funding necessary medical treatment

How Quickly Changes Affect Payments?

Changes in my savings affect my Universal Credit from the start of the next assessment period after the change happens. This means if I receive a lump sum halfway through an assessment period, it will not reduce my payment for that period but will apply to the next one.

The Importance Of Reporting Changes Promptly

I am legally required to report any change in my money, savings, or investments as soon as it happens. If I fail to report it:

- I could be overpaid and have to repay the money

- I may face a penalty for not reporting promptly

- In serious cases, it could be treated as benefit fraud

Reporting is done through my online Universal Credit account by selecting “Report a change of circumstances” and updating the “Money, savings and investments” section.

Are There Exemptions To The Universal Credit Savings Rules?

Certain types of capital are not counted either permanently or for a set period. These include:

- Personal injury and illness compensation (ignored for 12 months unless in a trust or used for an annuity)

- Bereavement Support Payments

- Funds from selling my main home, ignored for six months if buying another home

- Welfare payments and special compensation schemes such as Grenfell Tower or Infected Blood

These rules ensure that certain payments made for specific hardships do not unfairly reduce benefit entitlements.

Conclusion

The Universal Credit savings limit is a crucial factor in determining both eligibility and payment amounts.

By understanding what counts as capital, how it’s assessed, and the rules on reporting changes, I can make informed decisions and avoid unexpected reductions.

Staying transparent with DWP and managing my savings responsibly ensures my claim remains accurate and compliant.

FAQs

Can I get Universal Credit if I have £10,000 in savings?

Yes, but your payment will be reduced due to the tariff income calculation between £6,000 and £16,000.

Do premium bonds count as savings for Universal Credit?

Yes. Premium Bonds are classed as capital and are included in your savings assessment.

How does inheritance affect my Universal Credit?

Any inheritance counts as capital from the date it is received and must be reported immediately.

Is my pension considered savings for Universal Credit?

If it’s a lump-sum payment from a pension, it is treated as capital. Ongoing pension income is counted as income.

Do student loans count towards the savings limit?

Student loans are not treated as capital while being used for study-related expenses, but unspent amounts can be counted if retained after the assessment period.

How quickly will my Universal Credit stop if I go over £16,000?

Your entitlement usually ends from the assessment period in which your capital first exceeds £16,000.

Can I claim Universal Credit if my savings are tied up in property?

Yes, but only if it’s your main home or falls under an exemption such as housing a dependent relative. Otherwise, it is treated as capital.